morgages...how do they work?

03-06-2008, 10:06 AM

03-06-2008, 10:06 AM

#41

that's what gets me about the property market. you have only made that money is if you sell it for that  at this time you have potentially made it, but as you say it all depends on the market and in the end you could end up losing on it (although not likely in the long term)

at this time you have potentially made it, but as you say it all depends on the market and in the end you could end up losing on it (although not likely in the long term)

03-06-2008, 10:08 AM

03-06-2008, 10:08 AM

#42

PassionFord Regular

Join Date: Feb 2005

Location: Medway / Maidstone, Kent

Posts: 456

Likes: 0

Received 0 Likes

on

0 Posts

that's what gets me about the property market. you have only made that money is if you sell it for that at this time you have potentially made it, but as you say it all depends on the market and in the end you could end up losing on it (although not likely in the long term)

a) It was bought as an investment (and is not your normal residence) or

b) you downgrade your house at the top of the cycle.

With a), you obviously see the increase in capital, and with b), you have moved to a house which will fall less in value than your previous, more expensive house.

Increasing house prices are actually bad for people who want to upgrade because it moves the "rungs on the ladder" further apart.

Chip - hyperinflation isn't too comparable with houses and mortgages, but I see your point, if extreme!

The UK actually risks deflation in the next few years, as energy and food prices start to decrease and UK industry suffers from the US and EU slowdown.

Last edited by Ex-Finesse; 03-06-2008 at 10:11 AM.

03-06-2008, 10:18 AM

#43

Testing the future

or any zimbabwean now

i don't get that if they're getting extra rent on a mortgage that they took out a while ago, surely they are winning and it doesn't matter in the long term if the value is going down in the short term?

and if rental charges can be increased but property values are going down, surely that would be a good time to think about buy to let as the lower the value, the lower the repayments needed on a new mortgage?

and if rental charges can be increased but property values are going down, surely that would be a good time to think about buy to let as the lower the value, the lower the repayments needed on a new mortgage?

03-06-2008, 10:22 AM

#44

PassionFord Post Whore!!

phil by the sounds of it you would be better looking at the mortages with the oneaccount there realy only good if you can put away a bit extra every month or so.everybit you pay on top of your monthly payment comes of interest free.or sumthing like that lol.worth looking at tho im sure.

03-06-2008, 10:23 AM

#45

Id not bother getting a new buy to let property at the moment personally, the sums just dont really work very well at the moment (im sure comedy dan will try and disagree though, as im sure there are exceptions, lol) id say that its a "hold" market essentially.

03-06-2008, 10:24 AM

#46

phil by the sounds of it you would be better looking at the mortages with the oneaccount there realy only good if you can put away a bit extra every month or so.everybit you pay on top of your monthly payment comes of interest free.or sumthing like that lol.worth looking at tho im sure.

03-06-2008, 10:38 AM

#47

PassionFord Regular

Join Date: Feb 2005

Location: Medway / Maidstone, Kent

Posts: 456

Likes: 0

Received 0 Likes

on

0 Posts

i don't get that if they're getting extra rent on a mortgage that they took out a while ago, surely they are winning and it doesn't matter in the long term if the value is going down in the short term?

and if rental charges can be increased but property values are going down, surely that would be a good time to think about buy to let as the lower the value, the lower the repayments needed on a new mortgage?

and if rental charges can be increased but property values are going down, surely that would be a good time to think about buy to let as the lower the value, the lower the repayments needed on a new mortgage?

The property market is the slowest moving market I can think of. Downturns occur for years, not months.

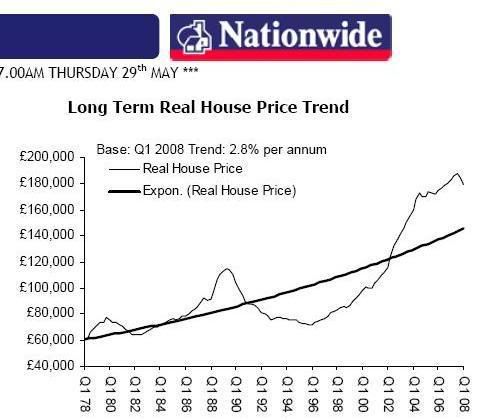

I estimate it will be 4 to 5 years before a property is up back to it's value at end of 2007 (the peak). Look below, if one bought in 1980, it takes until 1986 until it's the same price. Look at 1990, it takes until 2002 to become the same price!

That ignores the inflation that reduces the value of that money over the 4 to 5 years.

I estimate it will be 6 to 8 years before properties return to their current value, this time allowing for inflation.

That's the most recent Nationwide data. Look how long the downturns last. It takes even longer for the prices to recover... in which time the money could have been earning interest in a bank account, at worst!

Last edited by Ex-Finesse; 03-06-2008 at 10:41 AM.

03-06-2008, 10:49 AM

03-06-2008, 10:49 AM

#49

They are winning for the extra rent (say average �100 p/m) but they are equally loosing �1,000 p/m on the value of the property.

The property market is the slowest moving market I can think of. Downturns occur for years, not months.

I estimate it will be 4 to 5 years before a property is up back to it's value at end of 2007 (the peak). Look below, if one bought in 1980, it takes until 1986 until it's the same price. Look at 1990, it takes until 2002 to become the same price!

That ignores the inflation that reduces the value of that money over the 4 to 5 years.

I estimate it will be 6 to 8 years before properties return to their current value, this time allowing for inflation.

That's the most recent Nationwide data. Look how long the downturns last. It takes even longer for the prices to recover... in which time the money could have been earning interest in a bank account, at worst!

The property market is the slowest moving market I can think of. Downturns occur for years, not months.

I estimate it will be 4 to 5 years before a property is up back to it's value at end of 2007 (the peak). Look below, if one bought in 1980, it takes until 1986 until it's the same price. Look at 1990, it takes until 2002 to become the same price!

That ignores the inflation that reduces the value of that money over the 4 to 5 years.

I estimate it will be 6 to 8 years before properties return to their current value, this time allowing for inflation.

That's the most recent Nationwide data. Look how long the downturns last. It takes even longer for the prices to recover... in which time the money could have been earning interest in a bank account, at worst!

I suspect it may be significant and not just a blip, but its really too early to draw conclusions like the ones you are trying to draw.

03-06-2008, 11:16 AM

03-06-2008, 11:16 AM

#51

PassionFord Regular

Join Date: Feb 2005

Location: Medway / Maidstone, Kent

Posts: 456

Likes: 0

Received 0 Likes

on

0 Posts

You seem to have totally ignored all the small blips on the way up, where its gone down and then rapidly recovered and then exceeded the price before the downward blip, and TBH there just isnt the evidence yet that what we are experiencing now isnt just another of those in an otherwise steady rising market.

I suspect it may be significant and not just a blip, but its really too early to draw conclusions like the ones you are trying to draw.

I suspect it may be significant and not just a blip, but its really too early to draw conclusions like the ones you are trying to draw.

Look at the very recent downturn the graph shows. Nowhere else on the graph does that happen and prices jump back up. When that kind of drop occurs, it continues to drop for many years!!

No evidence to suggest we're not in a blip?

How about the data a few days ago of fewest mortgages ever approved for house sales in May? From memory, this was circa 54,000, and is about half the number at this point last year.

So imagine your market place, half the buyers, but no less sellers. If anything, number of sellers has increased. Prices will only go down if there's a shortage of buyers.

Abbey, Nationwide and HBOS have all increased their mortgage rates in the past few weeks. The credit crunch is far from over and mortgages will be harder to get over the next few months. We can expect to see new mortgages become less than half what it was last year.

Finally, yes the media do stoke fears of a slump. However the media were also responsible for driving the market up in the first place, with the endless programs and articles re. B-T-L and developing.

03-06-2008, 11:53 AM

#53

Money can only be made on the housing market if..

a) It was bought as an investment (and is not your normal residence) or

b) you downgrade your house at the top of the cycle.

With a), you obviously see the increase in capital, and with b), you have moved to a house which will fall less in value than your previous, more expensive house.

Increasing house prices are actually bad for people who want to upgrade because it moves the "rungs on the ladder" further apart.

Chip - hyperinflation isn't too comparable with houses and mortgages, but I see your point, if extreme!

The UK actually risks deflation in the next few years, as energy and food prices start to decrease and UK industry suffers from the US and EU slowdown.

a) It was bought as an investment (and is not your normal residence) or

b) you downgrade your house at the top of the cycle.

With a), you obviously see the increase in capital, and with b), you have moved to a house which will fall less in value than your previous, more expensive house.

Increasing house prices are actually bad for people who want to upgrade because it moves the "rungs on the ladder" further apart.

Chip - hyperinflation isn't too comparable with houses and mortgages, but I see your point, if extreme!

The UK actually risks deflation in the next few years, as energy and food prices start to decrease and UK industry suffers from the US and EU slowdown.

03-06-2008, 11:59 AM

#55

chip you have no chance as you have it on a buy to let explain your way out of that to the irs lol

Last edited by Turbosystems; 03-06-2008 at 12:00 PM.

03-06-2008, 12:04 PM

#56

15000

Join Date: May 2005

Posts: 43

Likes: 0

Received 0 Likes

on

0 Posts

Interesting thread this, as I am currntly looking to buy my first place! Couldn't have come at a worst time lol.

I really am in two minds as to what to do. I'm a FTB with a decent sized deposit, and have a property in mind. The mortage would be just over a weeks wage for me, so I wouldn't be making the mistake of mortgaging myself up to the hilt. Its up for �135k but I'd be pushing to get it at �125k.

On the other hand, I could get the property, the market could bottom out, and I could be in negative equity in a matter of months....

I really am in two minds as to what to do. I'm a FTB with a decent sized deposit, and have a property in mind. The mortage would be just over a weeks wage for me, so I wouldn't be making the mistake of mortgaging myself up to the hilt. Its up for �135k but I'd be pushing to get it at �125k.

On the other hand, I could get the property, the market could bottom out, and I could be in negative equity in a matter of months....

03-06-2008, 12:06 PM

#57

they are very strict on this it has to be your primary principal residence remember you are being watched by the inland revenue, you pop up on the land registry.minimum fine for non disclosure is 100% fine on the tax you owe max 400%

chip you have no chance as you have it on a buy to let explain your way out of that to the irs lol

chip you have no chance as you have it on a buy to let explain your way out of that to the irs lol

03-06-2008, 12:08 PM

#58

Interesting thread this, as I am currntly looking to buy my first place! Couldn't have come at a worst time lol.

I really am in two minds as to what to do. I'm a FTB with a decent sized deposit, and have a property in mind. The mortage would be just over a weeks wage for me, so I wouldn't be making the mistake of mortgaging myself up to the hilt. Its up for �135k but I'd be pushing to get it at �125k.

On the other hand, I could get the property, the market could bottom out, and I could be in negative equity in a matter of months....

I really am in two minds as to what to do. I'm a FTB with a decent sized deposit, and have a property in mind. The mortage would be just over a weeks wage for me, so I wouldn't be making the mistake of mortgaging myself up to the hilt. Its up for �135k but I'd be pushing to get it at �125k.

On the other hand, I could get the property, the market could bottom out, and I could be in negative equity in a matter of months....

03-06-2008, 12:15 PM

#59

Testing the future

exactly. as long as you have a good proportion of the value of the property as a deposit, you should have no problem getting a mortgage, and the rates are still relatively low. not the worst time to buy in history by any stretch of the imagination

03-06-2008, 12:49 PM

#60

15000

Join Date: May 2005

Posts: 43

Likes: 0

Received 0 Likes

on

0 Posts

Deposit would be 10-15%.

The other thing that I get hung up on is, why do we in the UK feel the need to own our homes? I see it two ways at the moment....

1) I buy somewhere with a 30-35 year mortgage. Pay it off in time for retirement and I then own my home. Whats the next move? Sell it, downsize and enjoy the money at the ripe old age of 65 or...

2) Rent somewhere for the same price per month a mortgage would be, getting a much nicer place. Buy a nice motor with some of my deposit and live for the now.

The other thing that I get hung up on is, why do we in the UK feel the need to own our homes? I see it two ways at the moment....

1) I buy somewhere with a 30-35 year mortgage. Pay it off in time for retirement and I then own my home. Whats the next move? Sell it, downsize and enjoy the money at the ripe old age of 65 or...

2) Rent somewhere for the same price per month a mortgage would be, getting a much nicer place. Buy a nice motor with some of my deposit and live for the now.

03-06-2008, 12:51 PM

#61

Deposit would be 10-15%.

The other thing that I get hung up on is, why do we in the UK feel the need to own our homes? I see it two ways at the moment....

1) I buy somewhere with a 30-35 year mortgage. Pay it off in time for retirement and I then own my home. Whats the next move? Sell it, downsize and enjoy the money at the ripe old age of 65 or...

2) Rent somewhere for the same price per month a mortgage would be, getting a much nicer place. Buy a nice motor with some of my deposit and live for the now.

The other thing that I get hung up on is, why do we in the UK feel the need to own our homes? I see it two ways at the moment....

1) I buy somewhere with a 30-35 year mortgage. Pay it off in time for retirement and I then own my home. Whats the next move? Sell it, downsize and enjoy the money at the ripe old age of 65 or...

2) Rent somewhere for the same price per month a mortgage would be, getting a much nicer place. Buy a nice motor with some of my deposit and live for the now.

If you rent though, you will rent the same place for 600 now, 800 in 5 years, 1200 in 10 years etc

So it doesnt take long before you start feeling poorer.

03-06-2008, 01:17 PM

#63

PassionFord Regular

Join Date: Feb 2005

Location: Medway / Maidstone, Kent

Posts: 456

Likes: 0

Received 0 Likes

on

0 Posts

All capital gains are now subject to 18%, so actually beneficial for the BTL crowd.

(*I can't remember if indexation allowance for individuals is still in force)

Also, was never really 40% after 2 years due to taper relief.

Very strict restrictions on Principal Private Residence exemption, as Mitsy said.

Lots of 90% mortgages still available, albeit higher rates than 75%.

I would hold fire on buying at the moment, unless one was particularly in love with a house, and couldn't care about the financial implications.

03-06-2008, 01:18 PM

#64

15000

Join Date: May 2005

Posts: 43

Likes: 0

Received 0 Likes

on

0 Posts

The fatal flaw in 2) is that if you get a 800 quid a month mortgage now, then give or take a bit with interest fluctuations, it will be 800 quid a month in 5 years and in 10 years and still in 25 years

If you rent though, you will rent the same place for 600 now, 800 in 5 years, 1200 in 10 years etc

So it doesnt take long before you start feeling poorer.

If you rent though, you will rent the same place for 600 now, 800 in 5 years, 1200 in 10 years etc

So it doesnt take long before you start feeling poorer.

Hi Ralph - Its Pete from Evo.

Last edited by 325Pete; 03-06-2008 at 01:19 PM.

03-06-2008, 01:25 PM

#65

Going for a short term deal never works out, they HAVE to make the cost up in other details, like higher arrangement fees or charging you to close the account etc, the reality is that they never save you much money if you do the maths.

some of the comparison sites do a whole life cost, and you will be amazed how little it varies on the different deals from the same lender even though it looks so different at first glance.

03-06-2008, 01:32 PM

#66

15000

Join Date: May 2005

Posts: 43

Likes: 0

Received 0 Likes

on

0 Posts

Hmm, I may have to look out for that! High Street deals have been around abouts 5.4% for 3/5 years then shoot up to app.7.2% for the remainder. Haven't really looked into the cost over the life of the mortgage.

03-06-2008, 01:42 PM

#68

Ban[B][/B]ned

Join Date: Jul 2005

Location: The Pool.

Posts: 34,090

Likes: 0

Received 0 Likes

on

0 Posts

03-06-2008, 03:41 PM

03-06-2008, 03:41 PM

#69

Too many posts.. I need a life!!

Join Date: Jan 2005

Location: Southampton

Posts: 790

Likes: 0

Received 0 Likes

on

0 Posts

brought mine jan last year if i sold last summer id have made 30k after id done it up (everything bar the front door) now its more like 20-25k and dropping... concerning but in the long run i cant see neg eq staying? well im hoping not!!

03-06-2008, 03:47 PM

#70

The problem that I see, is in the town that I live in, in the 1960s a 2 bed end of terrace was worth 5-6K and average wages were around 2K

Now, the same house is worth 200K, and average wages are around 15K

So it used to be 3 years wages to buy a house, its now more like 13!

There are of course many other factors than just that, but that is a frigthening statistic by any standards IMHO!

03-06-2008, 04:28 PM

#71

Guest

Posts: n/a

its all grim for the forseable houses have hit thier ceiling in the uk all you lot saying thier will never be a crash what ya sayin now? my cousins lost 25k on his house in 6 months and is now in neg and its only the beginning fuckinel im glad i waited i aint buying im building my own

03-06-2008, 04:38 PM

03-06-2008, 04:38 PM

#73

PassionFord Post Troll

Oh for a crystal ball.

03-06-2008, 04:52 PM

03-06-2008, 04:52 PM

#74

Guest

Posts: n/a

Negative equity only matter if he looses his job. If he's in a safe job, no worries. Thats what fucked everything in the early nineties, massive job losses coupled with negative equity. And given we are a more service based economy than manufacturing........ could be worse this time round, then again, it might all be fine.

Oh for a crystal ball.

Oh for a crystal ball.

Also back in the boom and bust days weren't mortgage rates something like 12-14%? at least currently you can still remortgage pretty comfortably if your earnings are the same, fuck having a mortgage back then!!

03-06-2008, 04:55 PM

#75

Precisely, its only an issue if he were planning on selling, he'll just have to stay there for a while now until the market turns again.

Also back in the boom and bust days weren't mortgage rates something like 12-14%? at least currently you can still remortgage pretty comfortably if your earnings are the same, fuck having a mortgage back then!!

Also back in the boom and bust days weren't mortgage rates something like 12-14%? at least currently you can still remortgage pretty comfortably if your earnings are the same, fuck having a mortgage back then!!

So a 7% mortgage now actually costs you MORE per month than it did in the 80s at 12%, and earnings havent actually gone up by a massive amount since the late 80s either, so in real terms, its actually about the same I should think!

03-06-2008, 05:08 PM

#76

Guest

Posts: n/a

Negative equity only matter if he looses his job. If he's in a safe job, no worries. Thats what fucked everything in the early nineties, massive job losses coupled with negative equity. And given we are a more service based economy than manufacturing........ could be worse this time round, then again, it might all be fine.

Oh for a crystal ball.

Oh for a crystal ball.

03-06-2008, 05:10 PM

#77

Guest

Posts: n/a

Fair enough Chip, I was thinking more along the lines of folks who fixed it when it was low and were facing 12-14% when their deal ended, although I'll admit I'm not that clued up on the ins and outs of the 80's mortgage industry as I was about 8 at the time

03-06-2008, 05:18 PM

#78

My parents fixed their's in the 70s, at 6% for the full term of the loan, their friends nearly all took the cheaper option and had 5% or so on variable and thought they were mad.

By the late 80s my parents friend's all changed their minds, lol

By the late 80s my parents friend's all changed their minds, lol

Thread

Thread Starter

Forum

Replies

Last Post

JK12

Pictures, video & Photoshop Forum

33

26-04-2021 12:09 PM

Rstar_man

Restorations, Rebuilds & Projects.

143

20-07-2020 11:16 PM